Mie Gacoan Business Model Canvas

Explore the Mie Gacoan Business Model Canvas, including its customer segments, value propositions, revenue streams, operations, competitive advantages, risks, and strategic recommendations.

Explore the Touch n Go Business Model Canvas, including its nine BMC blocks, Value Proposition Canvas, competitive advantages, risks, Boost comparison, and 2026 strategy. The Touch n Go BMC showcases how each building block contributed to that transformation. Through its customer-focused digital wallet, the company has successfully integrated payments, investments, and micro-insurance into a seamless experience.

BMC Article No: BMC #053

Updated in 2026: This article has been refreshed with Touch ’n Go Digital’s latest profitability milestone, the growing contribution of services beyond payments, cross-border payment expansion, newer merchant and business solutions, deeper analysis of all nine BMC blocks, a complete Value Proposition Canvas, an updated comparison with Boost, expanded competitive advantages and risks, and new strategic recommendations.

Touch ’n Go began as a familiar payment method for Malaysian toll roads and public transportation. Over time, the brand expanded beyond physical cards and mobility payments into a broader digital financial ecosystem covering retail payments, money transfers, rewards, investments, insurance, remittances, travel payments, merchant services, and other financial products.

The Touch n Go Business Model Canvas is strategically important because the company connects two powerful positions. Its transport heritage gives the brand strong everyday recognition, while TNG eWallet enables it to participate in Malaysia’s expanding digital economy.

Unlike a conventional payment application, Touch ’n Go increasingly operates as a platform that connects consumers, merchants, transportation networks, financial institutions, product providers, and international payment partners. Each additional service can increase customer engagement, transaction frequency, and opportunities for cross-selling.

This article examines how Touch ’n Go creates, delivers, and captures value. It also explains why the company’s transition from a payment utility into an integrated fintech platform could shape its next stage of growth.

Touch ’n Go operates a multi-sided payment and financial-services ecosystem. Consumers use its physical cards, RFID solutions, digital wallet, payment services, rewards, investment products, insurance solutions, travel features, and other embedded financial offerings.

Merchants benefit from payment acceptance, broader customer access, transaction tools, promotional opportunities, and business-account capabilities. Financial institutions and product partners gain access to a large digital user base through services integrated into the TNG eWallet platform.

At its core, the Touch n Go Business Model Canvas combines transaction infrastructure with platform economics. Payments bring users into the ecosystem, while financial services, merchant solutions, advertising, rewards, and partner products increase the value generated from each customer relationship.

Transport and toll payments remain valuable because they create frequent, habitual usage. Digital services then extend the relationship into more profitable areas such as investments, insurance, financing, remittances, and cross-border transactions.

This structure allows Touch ’n Go to evolve from earning primarily through payment activity into capturing value across a wider customer lifecycle.

Business Model Canvas, or BMC, is a strategic framework that explains how a company creates value, delivers that value to customers, and earns revenue from its activities.

The framework divides a business into nine connected building blocks. Instead of examining products in isolation, it shows how customers, technology, partnerships, operations, costs, and revenue mechanisms work together.

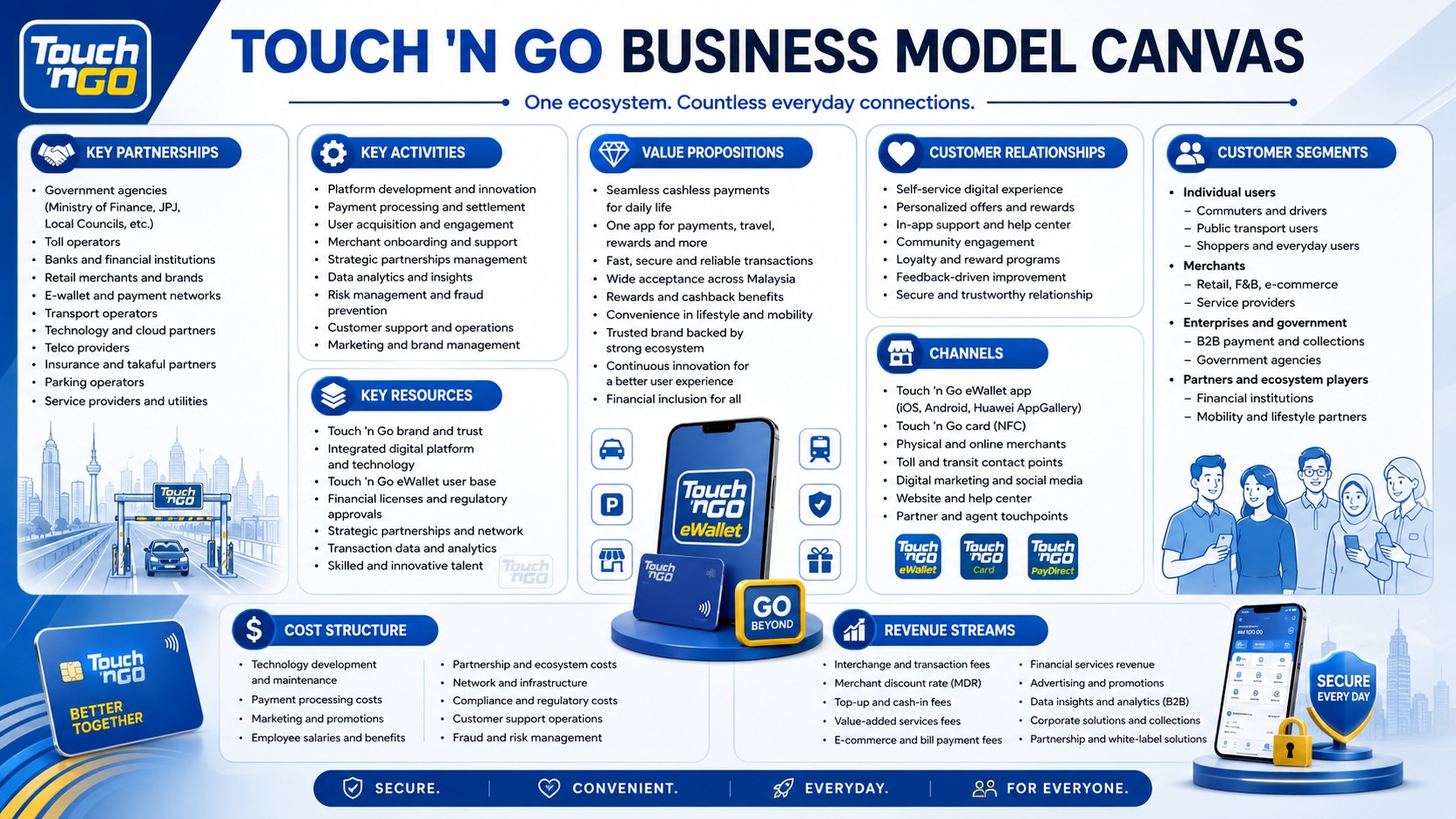

For Touch ’n Go, the Touch n Go Business Model Canvas helps explain how transport access, digital payments, merchant acceptance, financial products, data capabilities, and strategic partnerships reinforce one another.

| BMC Block | Main Question |

|---|---|

| Customer Segments | Who does the company serve? |

| Value Propositions | What value does it deliver? |

| Channels | How does it reach users and merchants? |

| Customer Relationships | How does it acquire and retain customers? |

| Revenue Streams | How does the company earn income? |

| Key Resources | What assets enable the model? |

| Key Activities | What must the company perform effectively? |

| Key Partnerships | Which external parties strengthen the ecosystem? |

| Cost Structure | What are the main operating costs? |

Touch ’n Go was originally associated with Malaysia’s electronic toll-collection system. The physical Touch ’n Go card later became widely used across toll roads, public transport, parking, and selected retail environments.

TNG Digital subsequently launched TNG eWallet, extending the brand into mobile payments and digital financial services. The application now supports everyday payments, peer-to-peer transfers, bills, prepaid services, rewards, travel-related transactions, investments, insurance, and merchant services.

More than 25 million Malaysians and residents reportedly trust the platform for payments and financial services. Its cross-border QR capability has also expanded, allowing users to transact in numerous overseas markets.

Recent performance indicates that the model is becoming commercially more mature. TNG Digital achieved its first annual profit, while services beyond payments grew to represent approximately half of company revenue.

That change is significant. It suggests that Touch ’n Go is no longer dependent only on payment volume and is gradually developing a more diversified fintech revenue base.

Touch ’n Go is strategically interesting because it transformed a transport-linked payment brand into a broader financial ecosystem without abandoning its original utility.

Many fintech companies must spend heavily to create daily usage. Touch ’n Go already benefits from habitual payment occasions associated with tolls, transportation, parking, retail purchases, and money transfers.

That foundation reduces customer-acquisition friction. Once users enter the ecosystem for payments, the company can introduce rewards, investments, insurance, remittances, merchant services, and travel-related features.

Another advantage comes from local familiarity. The brand is closely connected with Malaysian mobility and cashless payments, giving it a level of recognition that newer digital platforms may struggle to replicate.

However, familiarity alone does not guarantee long-term leadership. Touch ’n Go must continue turning frequent payment activity into deeper financial relationships while preserving security, reliability, affordability, and customer trust.

Several developments are reshaping the Touch n Go Business Model Canvas in 2026.

First, the company has reached an important profitability milestone. Its first annual profit indicates that operating scale and revenue diversification are beginning to support a more sustainable commercial model.

Second, non-payment services now contribute a much larger share of revenue. Investments, insurance, lending-related services, remittances, merchant solutions, rewards, and other financial offerings are becoming central rather than supplementary.

Third, cross-border usage is growing rapidly. Regional QR connectivity and international payment partnerships allow TNG eWallet to follow Malaysian users into overseas travel and spending occasions.

Fourth, merchant capabilities are expanding. The introduction of business-account services for SMEs, freelancers, online sellers, and smaller merchants extends the platform from consumer payments into business financial management.

Finally, security expectations are increasing. As Touch ’n Go handles more financial activities, fraud prevention, account protection, operational resilience, and customer education become critical parts of its value proposition.

Together, these developments show a company moving from wallet adoption toward ecosystem monetisation and deeper customer relationships.

The following summary provides a concise view of how Touch ’n Go’s major business components work together before the detailed analysis.

| BMC Block | Touch ’n Go Application |

|---|---|

| Customer Segments | Consumers, commuters, drivers, travellers, merchants, SMEs, gig workers, tourists, financial institutions, and government-linked partners |

| Value Propositions | Convenient payments, transport integration, broad merchant acceptance, financial access, rewards, and integrated everyday services |

| Channels | TNG eWallet, physical cards, RFID, merchant QR, payment terminals, websites, partner platforms, and customer-service channels |

| Customer Relationships | Self-service, rewards, promotions, personalised offers, security education, customer support, and merchant engagement |

| Revenue Streams | Transaction fees, merchant services, financial-product commissions, investment and insurance distribution, remittances, advertising, and partner income |

| Key Resources | Brand, user base, payment infrastructure, licences, technology platforms, transaction data, merchant network, and skilled workforce |

| Key Activities | Payment processing, product development, cybersecurity, compliance, merchant acquisition, partner integration, marketing, and risk management |

| Key Partnerships | Banks, PayNet, transport operators, toll concessionaires, merchants, insurers, asset managers, technology providers, and overseas payment networks |

| Cost Structure | Technology, cybersecurity, compliance, customer incentives, marketing, personnel, infrastructure, partner fees, and customer support |

The diagram below should provide a visual summary of the nine components. It can help readers understand how Touch ’n Go’s transport infrastructure, digital platform, partner ecosystem, and financial products operate as one connected business model.

The Touch n Go Business Model Canvas reveals that the company’s strongest feature is not a single payment product. Its advantage comes from integrating mobility, payments, merchants, financial services, and daily consumer activity within one ecosystem.

Each block contributes differently. Customer scale produces transaction volume, broad acceptance improves utility, trusted infrastructure supports adoption, and embedded products create additional revenue opportunities.

Customer segments identify the consumers, businesses, and institutional stakeholders served by Touch ’n Go. Although the company reaches a broad mass market, different groups enter the platform for different reasons.

Drivers may primarily use toll and RFID services. Urban commuters depend on transport payments, while everyday consumers use TNG eWallet for shopping, bills, transfers, and rewards.

Merchants and SMEs represent another important segment. Their participation increases payment acceptance and strengthens the usefulness of the platform for consumers.

| Segment | Details | Why It Matters |

|---|---|---|

| Everyday consumers | Individuals using the wallet for retail purchases, bills, transfers, reloads, rewards, and digital services | Generates recurring transaction volume and supports cross-selling |

| Drivers and commuters | Users paying for tolls, public transport, parking, and other mobility-related services | Creates habitual usage connected to essential daily activities |

| Travellers and tourists | Malaysians spending overseas and international visitors making local payments | Expands transaction occasions beyond domestic everyday spending |

| Merchants and SMEs | Retailers, food outlets, freelancers, online sellers, roadside traders, and growing businesses | Increases acceptance, transaction density, and merchant-service revenue |

| Institutional partners | Banks, transport operators, government agencies, insurers, asset managers, and other service providers | Adds capabilities, regulatory access, infrastructure, and financial products |

This segmentation creates a reinforcing network. More consumers attract merchants, while greater merchant acceptance makes the platform more useful to consumers.

The Touch n Go Business Model Canvas is particularly strong because it serves both the demand side and supply side of the payment ecosystem. Institutional partnerships then add services that neither side could obtain from a basic wallet alone.

The value proposition explains why customers and partners choose Touch ’n Go instead of relying entirely on cash, cards, banking applications, or competing wallets.

Convenience is the most visible benefit. Users can perform multiple activities through one application, reducing the need to switch between separate payment and financial platforms.

Familiarity strengthens that convenience. Many Malaysians already associate Touch ’n Go with trusted daily payment infrastructure.

| Value Proposition | Details | Why It Matters |

|---|---|---|

| Integrated daily payments | Supports retail purchases, transport, tolls, parking, bills, transfers, and online transactions | Makes the platform relevant across frequent everyday occasions |

| Mobility integration | Connects cards, RFID, PayDirect, transport payments, and vehicle-related services | Differentiates Touch ’n Go from wallets without strong transport roots |

| Financial accessibility | Offers investments, insurance, remittances, rewards, and other financial services within the app | Broadens financial participation and increases customer value |

| Wide acceptance | Works through merchant QR, DuitNow QR, partner networks, and overseas payment arrangements | Reduces payment friction and increases practical utility |

| Local relevance | Products, campaigns, language options, and services are designed around Malaysian consumer behaviour | Strengthens familiarity, usability, and market trust |

Touch ’n Go’s real proposition is the consolidation of daily financial activity. A customer can travel, pay, transfer funds, earn rewards, protect assets, and access investment options within the same ecosystem.

That breadth encourages users to see the platform as an everyday financial companion rather than an occasional payment tool.

Channels describe how Touch ’n Go acquires customers, distributes services, supports transactions, and communicates with its ecosystem.

The TNG eWallet application is the central digital channel. Physical cards, RFID tags, toll infrastructure, public-transport access points, merchant QR codes, and payment terminals extend the company into the physical world.

Partner channels are equally important. Banks, retailers, travel networks, e-commerce platforms, government programmes, and payment networks provide distribution without requiring Touch ’n Go to own every customer touchpoint.

| Channel | Details | Why It Matters |

|---|---|---|

| TNG eWallet | Main interface for payments, transfers, rewards, travel, investments, insurance, and account management | Creates a direct digital relationship with users |

| Cards and RFID | Physical payment instruments used across toll, transport, parking, and selected retail environments | Preserves Touch ’n Go’s mobility advantage and offline relevance |

| Merchant network | DuitNow QR, TNG QR, terminals, online checkout, and other acceptance points | Converts digital balances into practical everyday spending |

| Partner platforms | Banks, transport operators, e-commerce services, financial providers, and government-linked programmes | Expands reach and functionality through shared infrastructure |

| Digital communication | Social media, email, in-app notifications, websites, help centres, and advertising | Supports education, promotion, engagement, and customer support |

The combination of physical and digital channels creates an omnichannel advantage. Users encounter the brand while driving, commuting, shopping, travelling, and managing money.

Such repeated exposure keeps Touch ’n Go close to high-frequency customer activity and reduces dependence on a single acquisition channel.

Customer relationships determine how Touch ’n Go attracts users, builds trust, encourages repeat usage, and increases the adoption of additional services.

Self-service is central to the operating model. Customers register, verify their identities, make payments, manage balances, purchase products, and review transactions through the application.

Rewards and promotions support engagement, while security controls and customer education protect confidence in the ecosystem.

| Relationship Type | Details | Why It Matters |

|---|---|---|

| Self-service relationship | Users independently manage transactions and financial features through the app | Supports scale without requiring equivalent growth in branch infrastructure |

| Rewards and loyalty | GOrewards, cashback, vouchers, campaigns, and partner promotions | Encourages spending frequency and reduces customer inactivity |

| Personalised engagement | In-app messages, product suggestions, reminders, and behaviour-based offers | Supports cross-selling and improves product relevance |

| Customer assistance | Help centre, chatbot, digital support, dispute handling, and service channels | Helps resolve payment issues and preserve trust |

| Security education | Scam alerts, account-protection guidance, device controls, and fraud-prevention messages | Reduces avoidable losses and strengthens confidence in digital finance |

Payment relationships are highly sensitive to service failure. A rejected transaction, delayed refund, account restriction, or suspected fraud can quickly damage trust.

Touch ’n Go therefore needs to balance automated scale with responsive problem resolution. Loyalty depends not only on rewards but also on how effectively the company manages critical customer moments.

Revenue streams explain how Touch ’n Go monetises payment activity, platform access, financial products, merchant relationships, and partner services.

Transaction-related income remains important, but the model is becoming more diversified. Non-payment services now represent a substantial part of revenue, demonstrating progress beyond basic wallet economics.

Financial products can generate commissions, referral fees, distribution income, servicing revenue, or revenue-sharing arrangements without requiring Touch ’n Go to manufacture every product directly.

| Revenue Stream | Details | Why It Matters |

|---|---|---|

| Payment and transaction income | Fees or commercial income associated with merchant payments, wallet activity, card usage, and processing services | Provides recurring revenue linked to transaction volume |

| Financial-product income | Commissions or shared income from investments, insurance, financing, and other embedded products | Improves revenue per user beyond payment activity |

| Merchant services | Business-account features, payment acceptance, merchant tools, promotional services, and related solutions | Builds a broader business-to-business revenue base |

| Remittance and cross-border services | Income associated with international transfers, overseas QR payments, and travel-related transactions | Extends monetisation into higher-value international use cases |

| Advertising and partnerships | Sponsored placements, promotions, rewards partnerships, and ecosystem campaigns | Monetises platform traffic and access to engaged users |

The Touch n Go Business Model Canvas becomes more attractive when non-payment income grows faster than the cost of maintaining the payment ecosystem.

Payments create frequency, but adjacent financial services can produce deeper margins and stronger lifetime customer value. The main challenge is achieving this growth without making the application confusing or encouraging unsuitable financial-product usage.

Key resources are the assets Touch ’n Go requires to operate reliably, comply with regulation, deliver services, and maintain its competitive position.

Brand recognition is one of the company’s most valuable intangible resources. Malaysia’s long familiarity with Touch ’n Go gives the organisation a foundation of awareness that would be expensive for a new entrant to build.

Technology and regulatory capabilities are equally essential. Payment infrastructure must remain secure, resilient, scalable, and available during periods of heavy transaction activity.

| Resource | Details | Why It Matters |

|---|---|---|

| Trusted brand | Strong association with tolls, transport, payments, and Malaysian daily life | Reduces adoption friction and strengthens customer recall |

| Large user ecosystem | Millions of registered users generating transactions and behavioural data | Supports network effects, partnerships, and product distribution |

| Payment infrastructure | Wallet systems, processing platforms, card services, RFID capabilities, APIs, and merchant connectivity | Enables reliable transactions across physical and digital environments |

| Licences and compliance capability | Regulatory approvals, governance processes, risk controls, and compliance expertise | Allows the company to operate within the financial-services sector |

| Data and analytics | Transaction information, customer behaviour, merchant patterns, fraud indicators, and product insights | Improves risk management, personalisation, and commercial decisions |

| People and partnerships | Technology specialists, product teams, cybersecurity professionals, financial partners, and merchants | Provides expertise and capabilities that cannot be created by technology alone |

These resources are difficult to replicate as a complete system. A competitor may build an application, but reproducing Touch ’n Go’s brand, transport integration, user reach, merchant coverage, regulatory experience, and partnerships would require substantial time and capital.

Key activities represent the work Touch ’n Go must perform consistently to keep the ecosystem operating and growing.

Payment processing is the foundation. Transactions must be accurate, fast, secure, and available across multiple channels.

Product development extends that foundation into new use cases. Teams must design services that improve engagement without creating unnecessary complexity.

| Activity | Details | Why It Matters |

|---|---|---|

| Payment operations | Processing wallet, card, RFID, QR, transfer, and merchant transactions | Maintains the company’s core customer promise |

| Product development | Building and improving payment, travel, investment, insurance, rewards, and business features | Supports differentiation and future revenue growth |

| Cybersecurity and fraud management | Monitoring transactions, preventing account takeover, detecting scams, and responding to incidents | Protects customers, reputation, and regulatory standing |

| Regulatory compliance | Managing customer verification, anti-money-laundering controls, consumer protection, reporting, and partner oversight | Enables sustainable participation in financial services |

| Merchant and partner integration | Onboarding merchants, maintaining APIs, supporting payment acceptance, and connecting product providers | Expands ecosystem utility and transaction volume |

| Marketing and engagement | Running campaigns, rewards, financial education, cross-selling, and customer communications | Encourages adoption, retention, and broader product usage |

Operational excellence is critical because fintech growth can amplify both value and risk. Higher transaction volume creates more revenue opportunities, but it also increases exposure to fraud, outages, complaints, and regulatory scrutiny.

Touch ’n Go must therefore innovate without weakening the reliability of its core payment infrastructure.

Partnerships allow Touch ’n Go to offer capabilities beyond what it could efficiently build alone.

Banks and payment networks support fund movement and interoperability. Transport operators, toll concessionaires, and parking providers maintain the company’s mobility relevance.

Insurers, asset managers, remittance providers, and other regulated institutions supply financial products that Touch ’n Go can distribute through its digital platform.

| Partner Category | Details | Why It Matters |

|---|---|---|

| Financial institutions | Banks, payment processors, fund managers, insurers, lenders, and remittance providers | Adds regulated products and financial infrastructure |

| Payment networks | PayNet, DuitNow QR participants, card networks, and international payment partners | Expands domestic and overseas interoperability |

| Mobility partners | Toll operators, public-transport providers, parking operators, and vehicle-service partners | Protects Touch ’n Go’s transport-linked differentiation |

| Merchants and platforms | Retailers, restaurants, e-commerce platforms, billers, SMEs, and service providers | Increases transaction acceptance and everyday relevance |

| Government and regulators | Public agencies, regulatory bodies, and government-linked programme stakeholders | Supports compliance, inclusion initiatives, and national payment programmes |

| Technology providers | Cloud, cybersecurity, identity, analytics, telecommunications, and infrastructure vendors | Provides scale, security, reliability, and specialist technology |

Partnerships accelerate expansion, but they also create dependency. Product quality, customer service, security, and regulatory compliance can be affected by external parties.

Strong partner governance is therefore necessary. Touch ’n Go must ensure that ecosystem growth does not reduce accountability for the customer experience.

Touch ’n Go’s cost structure reflects the demands of operating a regulated, high-volume digital platform alongside physical payment infrastructure.

Technology spending includes software development, cloud services, transaction processing, integration, monitoring, storage, and system resilience.

Cybersecurity and compliance costs continue to rise as the company expands into more complex financial activities.

| Cost Category | Details | Why It Matters |

|---|---|---|

| Technology and infrastructure | Application development, cloud capacity, payment processing, system integration, maintenance, and resilience | Supports scale and transaction availability |

| Cybersecurity and fraud prevention | Monitoring, identity controls, fraud detection, security testing, incident response, and customer protection | Reduces financial loss and protects trust |

| Marketing and incentives | Cashback, rewards, vouchers, campaigns, merchant promotions, and customer acquisition | Drives usage but can weaken economics when overused |

| People and operations | Product teams, engineers, compliance professionals, customer support, risk specialists, and management | Provides the expertise needed to operate a complex ecosystem |

| Partner and network costs | Fees paid to payment networks, financial providers, technology vendors, and service partners | Enables products and market access without full internal ownership |

| Physical infrastructure | Cards, RFID components, distribution, replacement, service centres, and transport-related systems | Maintains the company’s physical mobility ecosystem |

Scale can spread fixed costs across a large transaction base. Nevertheless, profitability depends on controlling incentives, fraud losses, support costs, and partner expenses.

Long-term performance will improve when recurring non-payment revenue grows faster than platform and acquisition expenditure.

The Value Proposition Canvas examines how Touch ’n Go’s products match the practical jobs, frustrations, and desired outcomes of its customers.

While BMC explains the entire organisation, VPC focuses on customer fit. It asks whether Touch ’n Go is solving meaningful problems rather than simply adding more application features.

For the Touch n Go Business Model Canvas, this fit is strongest when the platform reduces friction in daily payments and then introduces relevant financial services at the right moment.

The customer profile reflects the needs of consumers who want simple, secure, and widely accepted ways to pay, travel, transfer money, manage everyday finances, and access selected financial products.

| Customer Profile | Details |

|---|---|

| Customer Jobs | Pay for tolls, transportation, parking, shopping, food, bills, and online services; transfer money; travel overseas; manage spending; access investments, insurance, rewards, and other financial products |

| Customer Pains | Carrying cash, managing multiple applications, slow transactions, limited merchant acceptance, reload difficulties, security concerns, scams, payment failures, unclear fees, and complex financial products |

| Customer Gains | Fast payments, broad acceptance, one-app convenience, trusted security, rewards, spending visibility, accessible financial services, smooth travel payments, and reliable customer support |

Customers do not necessarily want more features. Most want fewer steps, broader usability, clearer information, and confidence that their money is protected.

The strongest customer experience therefore comes from making complex payment and financial processes feel simple.

The value map shows how Touch ’n Go responds to customer needs through its product portfolio, pain relievers, and gain creators.

Its transport and payment infrastructure addresses frequent functional jobs. Financial products, rewards, and travel capabilities increase the value of remaining active within the ecosystem.

| Value Map | Details |

|---|---|

| Products and Services | TNG eWallet, physical cards, RFID, PayDirect, DuitNow QR payments, transfers, bill payments, reloads, rewards, investments, insurance, remittances, travel payments, Visa card services, and merchant accounts |

| Pain Relievers | Cashless payments, broad merchant acceptance, transport integration, digital transaction records, security controls, fraud monitoring, cross-border QR access, and centralised account management |

| Gain Creators | Cashback, loyalty points, vouchers, convenient mobility, integrated financial services, accessible investment entry points, personalised offers, international payment convenience, and business-management tools |

Touch ’n Go creates value by combining high-frequency utility with optional financial depth.

Customers may begin with toll or retail payments, then gradually adopt rewards, transfers, travel services, investments, or insurance as their confidence increases.

The following table links customer needs directly with the products and benefits delivered by Touch ’n Go.

| Customer Profile | Details | Matching Value Map | How Touch ’n Go Creates Fit |

|---|---|---|---|

| Customer Jobs | Customers need to pay, travel, transfer funds, manage daily expenses, and access selected financial services conveniently | Products and Services | Touch ’n Go combines physical mobility payments, digital transactions, merchant acceptance, travel services, and financial products within one ecosystem |

| Customer Pains | Users face cash inconvenience, fragmented applications, security threats, failed payments, limited acceptance, and complicated financial processes | Pain Relievers | The platform offers cashless transactions, broad QR acceptance, transport integration, account controls, transaction records, fraud monitoring, and digital support |

| Customer Gains | Customers want speed, reliability, rewards, convenience, trust, financial access, and smooth local or overseas payments | Gain Creators | Touch ’n Go delivers frequent payment utility, GOrewards, cashback, integrated financial products, travel capabilities, and personalised digital engagement |

Fit improves when a service is naturally connected to the customer’s immediate activity. Travel insurance is more relevant near an overseas trip, while merchant tools matter when a small business begins receiving frequent digital payments.

Contextual delivery can therefore create more value than displaying every product equally to every user.

The strongest fit occurs during high-frequency, low-friction activities.

A driver passes through a toll plaza using RFID. A commuter pays for public transport, while a consumer scans a QR code for lunch and later settles a bill through the application.

Further value emerges when those routine interactions lead to appropriate adjacent services. Travellers can make overseas payments, small merchants can manage business receipts, and consumers can access investment or insurance products without leaving the ecosystem.

Touch ’n Go’s challenge is maintaining simplicity as the platform expands. Too many competing features may weaken navigation and make the application appear commercially aggressive.

Clear customer journeys, transparent fees, strong security, and relevant recommendations are therefore essential to preserving product-market fit.

The following diagram should visually connect customer jobs, pains, and gains with Touch ’n Go’s products and services, pain relievers, and gain creators.

The Touch n Go Business Model Canvas is most appropriately compared with Boost because both are Malaysian fintech ecosystems familiar to local consumers and merchants, but Boost deserves added attention as more than a simple e-wallet rival. Boost has evolved from a payments-led platform into a broader fintech and digital-banking player with merchant services, embedded financing, cross-border ambitions, AI-driven capabilities, and Boost Bank, making the comparison more strategically relevant for readers who want to understand how two local fintech brands are expanding in different directions.

Touch ’n Go’s strategic centre is everyday payments supported by transport infrastructure, broad merchant acceptance, and a large consumer wallet ecosystem. Boost has increasingly positioned itself as a regional financial-technology and digital-banking group integrating its fintech application, merchant solutions, financing capabilities, cross-border services, and Boost Bank.

The difference is one of entry point and ecosystem direction. Touch ’n Go begins with mobility and payments before expanding into financial services. Boost places stronger emphasis on credit, merchant financing, artificial intelligence, and digital banking.

| Dimension | Touch ’n Go | Boost |

|---|---|---|

| Core strategic position | Everyday payment and mobility ecosystem | Integrated fintech and digital-banking ecosystem |

| Primary entry point | Toll, transport, retail payments, transfers, and wallet usage | Wallet, PayFlex, merchant services, financing, and digital banking |

| Distinctive advantage | Transport heritage, broad consumer recognition, extensive everyday payment utility | Digital-bank integration, financing capabilities, and merchant-focused fintech solutions |

| Financial-services model | Embeds investment, insurance, remittance, travel, and related services into a large wallet platform | Connects wallet activity with credit, merchant finance, AI-driven services, and banking |

| Merchant proposition | Payment acceptance, DuitNow QR reach, campaigns, and business-account tools | Payments, merchant services, financing, and broader business enablement |

| Growth direction | Deepen engagement, increase non-payment revenue, and expand cross-border utility | Build a regional digital-banking group and increase financial-product penetration |

Neither model is automatically superior. Touch ’n Go has stronger mobility-linked frequency and consumer payment familiarity, while Boost has a clearer digital-banking and financing orientation.

Touch ’n Go possesses several reinforcing advantages that make its ecosystem difficult to displace.

Together, these strengths create a business based on embedded daily utility rather than occasional promotional usage.

Touch ’n Go also faces significant risks as its ecosystem becomes larger and more financially complex.

These risks do not weaken the strategic logic of the model. They show that future growth must be supported by stronger trust, operational resilience, and customer protection.

Touch ’n Go should prioritise deeper customer value rather than pursuing feature volume alone.

First, management should simplify the application around a small number of customer journeys such as Pay, Travel, Grow, Protect, and Business. A clearer structure would improve product discovery without overwhelming users.

Second, fraud prevention should become a visible competitive differentiator. Real-time scam warnings, stronger beneficiary checks, configurable transaction limits, rapid account freezing, and dedicated fraud-case support could strengthen trust.

Third, merchant services should expand beyond payment collection. Cash-flow dashboards, automated reconciliation, e-invoice integration, inventory connections, payroll tools, and responsible financing referrals could increase SME loyalty.

Fourth, financial products should be delivered contextually. Insurance, investments, remittances, and financing options should appear when they are relevant to customer needs rather than through broad promotional exposure.

Fifth, cross-border capabilities should be developed into a complete travel proposition covering payments, foreign-exchange transparency, transport, insurance, rewards, and spending insights.

Sixth, Touch ’n Go should use loyalty data to reward ecosystem depth rather than simple spending. Customers using transport, retail payments, savings, and merchant services could receive differentiated benefits.

Finally, service recovery needs greater strategic attention. Faster dispute resolution and clearer status tracking can protect trust when technology or partner processes fail.

The Touch n Go Business Model Canvas explains how a Malaysian transport-payment brand has developed into a broad digital financial ecosystem.

Its foundation remains highly defensible. Toll roads, public transport, RFID, physical cards, merchant payments, and a large eWallet user base create frequent activity that many fintech competitors must spend heavily to generate.

Future growth, however, will depend less on payment adoption alone. Touch ’n Go must turn everyday transactions into trusted, relevant, and profitable relationships across financial services, travel, merchant solutions, and cross-border payments.

The company’s first annual profit and rising non-payment contribution suggest that this transition is already taking place. Continued success will require disciplined product design, stronger security, responsive customer support, effective partner governance, and careful monetisation.

Touch ’n Go can remain one of Malaysia’s most influential fintech platforms if it protects the simplicity and reliability that made the brand valuable while expanding into services that genuinely improve customers’ financial lives.

This article is provided for educational and business analysis purposes only. Its content is based on publicly available information, general market observations, and strategic interpretation. It does not constitute financial advice, investment advice, legal advice, or an official statement from Touch ’n Go Sdn Bhd, TNG Digital Sdn Bhd, or their related companies.

Readers should conduct their own research before making any business, investment, or strategic decisions. All trademarks, logos, copyrights, brand names, product names, and related materials mentioned or shown in this article belong to their respective owners.

Explore the Touch n Go Business Model Canvas, including its nine BMC blocks, Value Proposition Canvas, competitive advantages, risks, Boost comparison, and 2026 strategy.

Explore the Mie Gacoan Business Model Canvas, including its customer segments, value propositions, revenue streams,… Read More

Restaurant Business Model Canvas: A Practical Guide to Designing, Evaluating, and Improving Restaurant Business Models… Read More

Learn how the Food and Beverage Business Model Canvas helps restaurants, cafés, beverage brands, and… Read More

Read this Apple Business Model Canvas analysis to understand how Apple creates value through premium… Read More

This Business Model Canvas AWS analysis explains how the company creates, delivers, and captures value… Read More

Hermes Business Model Canvas explained in depth, including customer segments, value proposition, channels, revenue, competitive… Read More

{kind=link}

{kind=link}